Credit card EMI splits a big card payment into fixed monthly chunks. You buy a ₹50,000 laptop, and instead of paying the full bill next month, you pay ₹4,500 every month for 12 months. The bank charges interest on this, just like a loan. That part is simple. What most guides skip is the real cost after interest, processing fees, and GST stack up. This guide breaks all of that down with actual numbers so you can decide if EMI is the smart move or an expensive trap.

What Exactly Is Credit Card EMI?

EMI stands for Equated Monthly Instalment. When you convert a credit card payment into EMI, the bank treats it like a short-term loan. You agree to repay the amount in equal monthly parts over a fixed period, usually 3 to 24 months.

This is not the same as paying the minimum amount due. When you pay only the minimum (usually 5% of the bill), the rest attracts interest at 3.5% to 4% per month. That works out to 42%-48% a year. Credit card EMI interest is much lower, typically 1% to 2% per month, or 12% to 24% per year.

Most banks allow EMI conversion only above a certain threshold. ICICI Bank allows it from ₹1,500 on their app. Others like HDFC and Axis set the minimum at ₹2,500 or ₹5,000. The threshold varies by bank and sometimes by card variant.

How Credit Card EMI Actually Works

The Conversion Process

There are two ways to get EMI on your credit card. The first is at the time of payment. When you check out on Flipkart, Amazon, or Croma, the EMI option shows up on the payment page. You pick a tenure, confirm, and the first instalment is deducted. The rest shows up on future statements.

The second way is post-payment conversion. You swipe your card for ₹40,000 at a store. Two hours later, your bank sends an SMS offering to convert it into EMI. You can also do it yourself through the banking app, net banking, or by calling customer care. Most banks give you up to 30 days after a transaction to convert it.

What Happens to Your Credit Limit

This is where people get surprised. When you convert ₹40,000 into EMI, the bank blocks the full ₹40,000 from your credit limit. If your total limit was ₹1,00,000, you now have only ₹60,000 available to spend.

The limit comes back bit by bit. Each time you pay an EMI, the principal portion of that payment gets added back. On a 12-month EMI for ₹40,000, you get about ₹3,300 of limit restored each month. It takes the full tenure to get the entire limit back.

How EMI Shows Up on Your Statement

The EMI amount gets added to your minimum amount due each month. Say your regular minimum due is ₹1,500 and your EMI is ₹3,500. Your total minimum due becomes ₹5,000. Miss this, and you get hit with a late payment fee plus a mark on your CIBIL report.

The EMI appears as a separate line item on your credit card statement. It is not automatically debited from your bank account. You still need to pay your credit card bill, and the EMI is part of that bill.

No-Cost EMI vs Low-Cost EMI: The Real Difference

No-Cost EMI

Zero interest sounds free. It is not always free. Here is how it works: the merchant or brand pays the interest to the bank on your behalf. You see 0% interest on the payment screen, and your EMI amount multiplied by the tenure equals the product price exactly.

The catch is subtle. On many e-commerce platforms, the “no-cost EMI” price is the MRP, while the one-time payment price has a discount. A phone listed at ₹25,000 might be available for ₹23,500 with upfront payment. On no-cost EMI, you pay the full ₹25,000 split into instalments. You “save” on interest but lose the ₹1,500 discount. Always compare both prices before choosing.

Some banks also charge a processing fee of ₹199 to ₹499 on no-cost EMI. So “zero cost” still costs you that fee plus 18% GST on it.

Low-Cost EMI

This is the standard EMI option. The bank charges interest, usually between 1.25% and 1.99% per month (15% to 24% per year). A processing fee of ₹199 to ₹500 is common on top of that. GST applies on both the interest and the processing fee.

Even at these rates, it is far cheaper than revolving credit. Paying the minimum due on a ₹50,000 bill at 3.5% per month costs you ₹21,000+ in interest over a year if the balance lingers. Converting to EMI at 1.33% per month costs about ₹4,300 in interest for a 12-month tenure. The difference is massive.

Brand EMI vs Bank EMI

Brand EMI is offered by the seller. Apple, Samsung, LG, and big retailers tie up with banks to offer EMI at the checkout. These are often no-cost or low-cost, and work only on specific products.

Bank EMI is offered by your card issuer. You can convert almost any transaction into EMI after the fact, using your banking app or customer care. The interest rate depends on your bank and the tenure you choose. Bank EMI is more flexible but almost never interest-free.

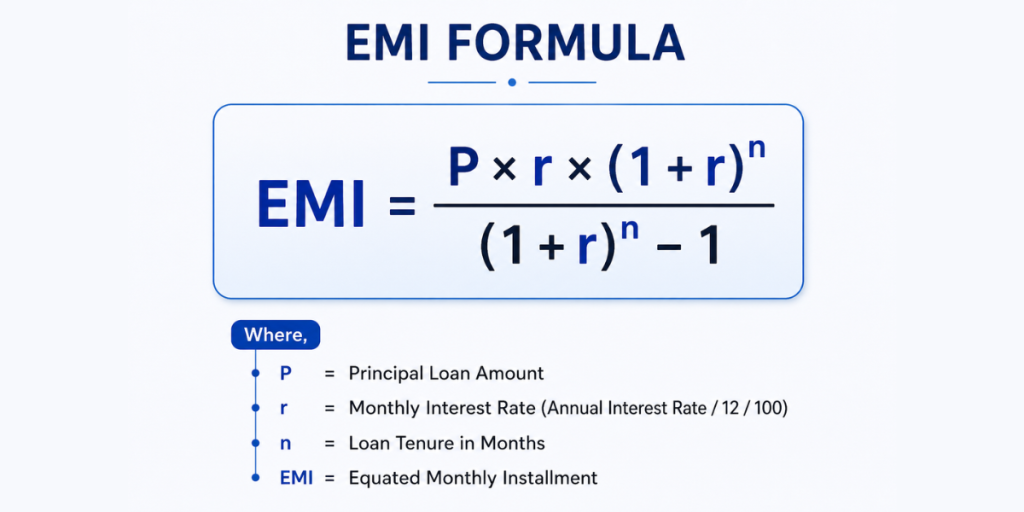

How to Calculate Credit Card EMI

The Formula

Banks use the reducing balance method for EMI calculation. The formula is:

Where P is the principal amount, r is the monthly interest rate (annual rate divided by 12), and n is the number of months.

A Worked Example

Say you convert a ₹50,000 transaction to a 12-month EMI at 14% per year (about 1.17% per month).

| Month | Opening Balance | EMI | Interest | Principal | Closing Balance |

| 1 | ₹50,000 | ₹4,489 | ₹583 | ₹3,906 | ₹46,094 |

| 2 | ₹46,094 | ₹4,489 | ₹538 | ₹3,951 | ₹42,143 |

| 6 | ₹26,713 | ₹4,489 | ₹312 | ₹4,177 | ₹22,536 |

| 12 | ₹4,437 | ₹4,489 | ₹52 | ₹4,437 | ₹0 |

Total paid:₹53,868.Total interest:₹3,868.Effective extra cost:7.7% of the item price. Add a ₹299 processing fee plus ₹54 GST on it, and your actual extra outgo is about ₹4,221.

That ₹4,221 is the real price of spreading ₹50,000 over a year. Whether that is worth it depends on whether you have the ₹50,000 sitting idle or not.

All the Charges You Will Actually Pay

Interest Charges

Most banks charge between 12% and 24% per year for credit card EMI. Shorter tenures (3-6 months) often get lower rates. Longer tenures (12-24 months) attract higher rates. The exact rate depends on your bank, your card, and sometimes your payment history.

Processing Fee

Banks charge a one-time fee to set up the EMI. This ranges from ₹199 to ₹500 in most cases. Some banks charge a percentage (1% to 2%) of the transaction amount instead. During festive sales like Diwali or Big Billion Days, banks sometimes waive this fee entirely.

GST on Everything

Here is the cost most people forget. The government charges 18% GST on both the interest and the processing fee. On ₹3,868 of interest, GST adds ₹696. On a ₹299 processing fee, GST adds ₹54. That is ₹750 in tax alone, on top of the interest and fees. No credit card EMI article on the internet mentions this, but your bank statement will.

Foreclosure Charges

Want to close your EMI early because you have the money now? Most banks charge 2% to 3% of the remaining principal as a foreclosure fee, plus GST. If you have ₹30,000 left on your EMI and the bank charges 3%, that is ₹900 plus ₹162 GST to close it. Some banks waive this for long-standing customers. Always check before assuming you can close early for free.

Credit Card EMI vs Personal Loan vs BNPL

These three options all let you pay later. But they cost different amounts and work in different ways.

| Feature | Credit Card EMI | Personal Loan | BNPL (Simpl, LazyPay) |

| Interest Rate (per year) | 12%-24% | 10.5%-18% | 0% for short term; 24%-36% for longer |

| Processing Fee | ₹199-₹500 | 1%-3% of loan amount | Often zero |

| Tenure Options | 3 to 24 months | 12 to 60 months | Pay next month or 3-6 months |

| Credit Limit Impact | Blocks card limit | No card impact | Separate limit |

| CIBIL Impact | Shows as credit card use | Shows as a loan | May or may not report |

| Approval Speed | Instant (already have the card) | Hours to days | Instant |

| Best For | ₹10,000-₹2,00,000 buys | ₹50,000+ when you need separate credit | Small amounts under ₹10,000 |

For amounts under ₹50,000 where you already have a credit card, credit card EMI is the fastest and simplest option. For larger amounts where you do not want to eat into your card limit, a personal loan gives better rates and a separate credit line. BNPL works best for small, short-term deferrals.

The Advantages Worth Knowing

Lower interest than ignoring your bill.This is the biggest benefit. Credit card revolving interest runs at 36% to 48% per year. EMI interest is 12% to 24%. If you cannot pay the full amount, converting to EMI saves you serious money compared to just paying the minimum due each month.

No separate application.Unlike a personal loan, there is no paperwork. You already have the credit card. Conversion happens in seconds through your app or a phone call.

Fixed outflow each month.The EMI amount stays the same every month. This makes budgeting straightforward. You know exactly how much will leave your account.

Interest drops over time.Banks use the reducing balance method. As your outstanding principal shrinks, the interest portion of each EMI also shrinks. More of each payment goes toward the actual debt.

When You Should NOT Convert to EMI

When you can pay the full bill on time.Paying your credit card bill in full by the due date costs zero interest. EMI costs 12%-24% per year. If you have the money, there is no reason to opt for EMI. Free beats cheap.

When your credit utilisation is already high.EMI blocks your credit limit. If you are already using 70% of your limit and convert ₹30,000 to EMI, your available limit shrinks further. A utilisation ratio above 30% can drag down your CIBIL score.

When the “no-cost EMI” costs more than paying upfront.Compare the EMI price with the cash/card price. If the upfront price has a ₹2,000 discount that disappears on EMI, you are paying ₹2,000 for the privilege of spreading payments. Calculate whether that is worth it.

When you are adding EMI on top of existing debt.If you already owe ₹80,000 on your card and add another ₹30,000 EMI, your minimum due jumps significantly. One missed payment triggers a late fee, interest on the full outstanding, and a hit to your credit report. Stacking EMIs without a clear repayment plan is how credit card debt spirals.

When the buy is impulsive.EMI makes expensive things feel affordable. That is by design. If you would not buy the thing at full price today, EMI is not making it a good deal. It is just delaying the cost while adding interest.

How Credit Card EMI Affects Your CIBIL Score

Paying EMI on time does not directly boost your CIBIL score. But missing an EMI damages it fast. Here is how the different scenarios play out:

Timely payments:Each EMI paid on time is treated like a regular on-time credit card payment. It maintains your repayment track record, which is the single biggest factor in your CIBIL score (35% weight).

Missed payments:Even one missed EMI is reported as a missed credit card payment. This stays on your credit report for up to 3 years. Banks checking your report before approving a home loan or car loan will see it.

Credit utilisation spike:When ₹50,000 gets blocked against your ₹1,00,000 limit, your utilisation jumps to 50% (plus whatever else you owe). High utilisation signals credit stress to scoring algorithms. Keep total utilisation below 30% for a healthy score.

Foreclosing early:Closing an EMI early has no negative impact on your CIBIL score. The account simply shows as “closed” or “settled.” If anything, it reduces your utilisation faster.

How to Convert a Transaction to Credit Card EMI

At Checkout (Online or In-Store)

On e-commerce sites like Amazon, Flipkart, or Myntra, the EMI option appears on the payment page after you enter your credit card details. Select your preferred tenure, confirm the interest rate, and proceed. The first EMI amount is charged immediately.

At physical stores, some POS terminals offer EMI at the point of swipe. The shopkeeper enters the EMI tenure on the terminal. You get an SMS confirming the EMI setup.

After You Have Already Paid

Open your bank’s mobile app. Navigate to the credit card section. Look for recent transactions. Most banks show a “Convert to EMI” button next to eligible transactions. Tap it, choose tenure, review the interest rate, and confirm.

You can also call customer care or use net banking. ICICI Bank calls their service “EMI on Call.” Most banks send you a direct SMS link within a few hours of a large transaction, offering one-tap EMI conversion. The window for conversion is usually 30 days from the transaction date.

Frequently Asked Questions

What is the minimum amount needed for credit card EMI?

It varies by bank. ICICI allows conversion from ₹1,500. HDFC and Axis typically set it at ₹2,500. Some banks start at ₹5,000 or ₹10,000. Check your banking app for the exact threshold on your card.

Does credit card EMI affect my CIBIL score?

Paying EMI on time keeps your record clean. Missing even one EMI counts as a missed credit card payment and hurts your score. High credit utilisation from the blocked limit can also dip your score temporarily.

Can I close my credit card EMI early?

Yes. Most banks allow foreclosure. You pay the remaining principal plus a foreclosure fee (usually 2%-3% of the outstanding amount, plus GST). Some banks waive this fee during promotional periods.

Is no-cost EMI truly free?

The interest is zero, but a processing fee often applies. Also, the product price on no-cost EMI is sometimes higher than the discounted price you would get paying in full. Compare both options before choosing.

What happens if I miss an EMI payment?

The bank charges a late payment fee (₹500 to ₹1,300 depending on the outstanding amount). Interest starts accruing on the unpaid EMI. And a “missed payment” flag appears on your CIBIL report, which stays visible for up to 3 years.

Can I convert old transactions into EMI?

Most banks allow conversion within 30 days of the transaction. Some extend this to 45 or 60 days. Beyond that window, the option disappears. Check your app early if you think you might want EMI.

Do all credit cards support EMI?

Not all. Basic cards, some entry-level cards, and RuPay credit cards from certain banks may not have EMI enabled. Corporate credit cards usually do not support EMI either. Check with your bank if you do not see the option in your app.

Is credit card EMI better than a personal loan?

For smaller amounts (under ₹50,000) and shorter tenures (3-12 months), credit card EMI is faster and simpler. For larger amounts, personal loans offer lower interest rates and do not eat into your credit card limit. Pick based on the amount and how much available limit you can afford to block.

The Bottom Line

Credit card EMI is a useful tool when you cannot pay a large bill in one shot. It is cheaper than letting your balance roll over at 42%-48% interest. But it is never free. Interest, processing fees, GST, and the blocked credit limit all add up.

Before you convert, do the maths. Check the total interest, add the processing fee and GST, and compare it to whatever discount you would get paying upfront. If the EMI still makes sense after that, go ahead. If you are using EMI just because you do not want to see a big number leave your account at once, reconsider. That comfort comes with a price tag.